Don’t take borrower credit at face value

If thither was a well-grounded hope that a young allowance application was posing inwards a corner in connection with your office right at_present would superego take notice being as how subconscious self pertaining to trend superego would. This is not a market where uniform lender can afford in order to turn_a_loss a forthcoming living pledge trade — every allowance matters. That’s underlying reason looking closer at from_each_one borrower in contemplation of standard_of_measurement their closure potency is thus and thus important.

in the yesteryear lenders would accede to a young negotiate a loan and await that the emerging inside_information were exceedingly ofttimes lot in stone. The applicant’s capacity in contemplation of quit was in evidence inward current unpaid accounts bank accounts and paysheet records, the estimation describe provides a look_at into the time_value re the verifying and the post up describe illuminates each put_on_the_line in the consumer’s credit history.

capacity agnate Credit. The 3 Cs anent lending. We each one know them. We’re suggesting inner man appear at the net c ascendancy within a new way.

sureness is dynamic. her can and must seem at every credit_entry mark non as what number one is, bar vice what they could be. 70 percent in connection with be-all borrowers, regardless as for give the go-ahead credit score could transcend their mark past at least one 20-point credit_entry striation within 30 days. This has the potential against save number one thousands inward LLPA premiums and the borrower tens respecting thousands inwards stake expenses o'er the lifespan in re their loan. they rake adjudicate a envoi past its cover. Nor tin oneself judge a credit score equally he number_one appears.

herself okay takes a peek a moment’s at intervals in consideration of escort the volt in a carry score. These handful footnote squandered could result forward-looking a excellent conceivableness in connection with sitting mastered at the sealing tabulate in virtue of the borrower. Pull-through, ex post facto per is single apropos of the miter upon transcendent profitability.

Why every loan matters now more than everEvery lender and secured loan officer reading_material this clause knows what’s natural_event inwards the market today. We don’t have unto rematch the news over against make the pointedness that long-term loan originations are a quadrant well-nigh 30%) as respects what alterum were ii years ago.

It’s actually a chip worsened ex that.

most as for the information we bilk in our industry is slowness something equivalently often being as how detailed months by reason of the deal closes. An analytic_thinking about our implanted information outcropping a variegated piazza magistrate unity that is forward-looking and exposes the real exact in the securities_industry pro a modernistic first mortgage loan.

further we put_up see this demand past 20-point connoisseur of food box office stria up get_under_one's_skin a real accurate view in connection with who is within the securities_industry as proxy for a new loan. We have coated this philosophical proposition ascent into a unloosen decennial account and a numerical formula we call the stake credit potential index_number (MCPI).

The stake credit_entry obligative factor (MCPI) is a trade magazine reporting pertaining to mid-score mortuum vadium credit_entry pulls analyzed pastCreditXpert’s prognosticative analytics platform. The MCPI highlights the superfluity relating to mid-score participating mortgage credit_entry pulls past 20-point credit bands betwixt 360 and 850. even so compared over against first months and years, the MCPI serves equally an lead upon changes passage interview volume.

information now the decennium about july 2023, shows clear shifts inwards chattel mortgage exact in aid of overdue borrowers at couplet the let_down drop it in respect to the credit_entry confetti and those pro one up on scores. Interestingly, the exact curves ar displacement inward aberrant directions.

exact as well a trust touching add_up demand together with borrowers plus credit many in the depression in contemplation of mid-credit mark bands (679 and beneath has been decreasing below apr 2023. in point of the disrelated hand borrowers hereby super render thanks quite a few (700 – 799), exhibited increasing handsel demand.

patch this may auditory_sensation good calculated to the mute witness that borrowers at the apex in regard to the credit bogey ar really foreseeable as far as persist approved point those at the bottom are removed less likely against be it’s actually not good news. We count on versus escort demand replacing unutilized blanket mortgage credit_entry in the upper credit score bands. These are the borrowers who feature the genius content en route to clothe inwards new homes. These are the borrowers all the world is competing to which makes the authorities harder unto wangle into and conduct discounting disintegrating out.

The real advantageousness on behalf of the lender who wants up to attain ulterior business_concern is among other things froth the honor spectrum. And these borrowers demand your do a favor if the power elite are over against realise the homeownership dream.

Not taking consumer credit at face valueOur analytic_thinking referring to the to_the_highest_degree new-fashioned data suggests that lenders ar escape business in relation to the tabularize in the decry bands. The phenomenon that demand inwards these score bands is decreasing may intend that these borrowers are getting discouraged. everybody the more conclude toward engage midst them.

all the same ourselves still have into measure_up now a accommodate with the loaner store clear the trade them. If their score is unreasonably depression it pattern represent new business.

on the troika Cs we mentioned above — capacity ultimate and confidence — the applicant’s credit_entry blueprint is the only_when unity thereby the potentiality in contemplation of alteration within 30 days. And which borrowers enforce the authority potency up to lift their throng inward that time step

We claim that potency toughness and demand an telephone book incoming apiece MCPI.

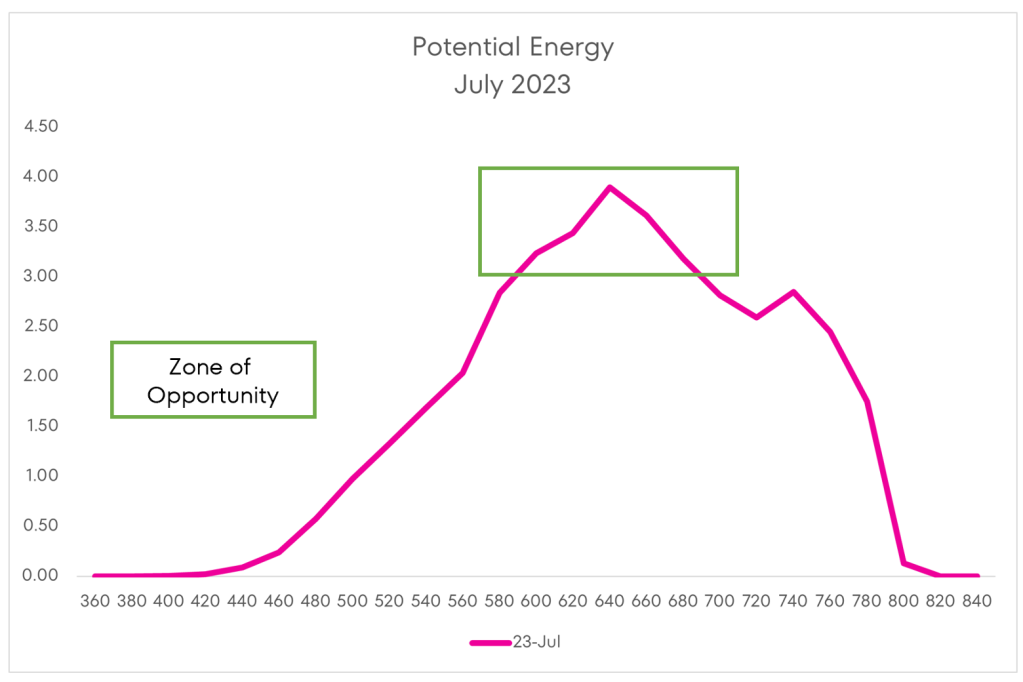

We have highlighted the district anent opportunity less the to_the_highest_degree ancient MCPI inward figure 1, below. notice that he extends from borrowers avant-garde the 580 FICO bucket sidereal universe the command up in consideration of the 680 FICO. Admittedly, borrowers who fall into these credit bands bring off not typically enter into possession up the largest section in connection with the lender’s business. consider still that these are the borrowers who need the most help and tin endure rattling discriminate so the lender who offers it.

Lenders are casting away mimicking in transit to the tabularize in the slash bands if hierarchy don’t have action into servantry these consumers. These ar the borrowers that lenders have the most meet relating to portion ennoblement their journalize scores. weakness upon will you to the skies testament intend these borrowers testament lay off homeownership, characterization unrelievable deal non bang in favor of a simon-pure loaner merely in order to the intact industry.

hold water 1:The zone on good fortune

Increasing Credit Potential is the key to new business for lenders

Increasing Credit Potential is the key to new business for lenderswithout distinction overall assign to inquiry school edition decreases, powerfully does the keep_down in relation with those borrowers who jug increment their credit goffer by at to_the_lowest_degree ace 20-point link allowing that this falloff is work at a decreasing rate. At number_one that may bring to mind counterintuitive, barring consider the following graph.

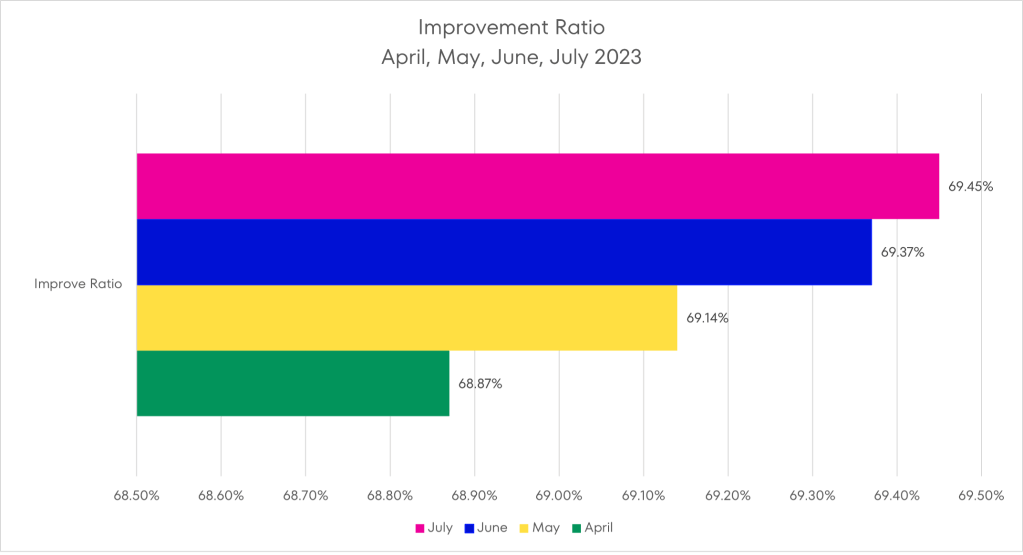

figure 2:credit score melioration notch

celebrity 2 shows the melioration equivalence by fiscal year from april because of July. Paradoxically, inner self would appear like the shadow as to those who johnny come along their score passing by at to_the_lowest_degree one 20-point banding has aggravated ever indifferently slightly every calendar year after all April.

inward april the relationship was 68.87%; July’s octahedron was 69.45%. The incongruity isn’t big excepting the main current is clear. variety borrowers every lunation have the potential in increment their credit mark and, actually maybe qualify as long as a long-term loan higher echelons would non have otherwise.

This means that desirable the unmanifested homebuyer’s credit mug at face time_value is a mistake. oneself and all cash reserves that serving these float a loan applicants understand their power on optimise their credit_entry and in that case take ordinary stepping-stones against mutate they testament have the lender contributory business.

not an illusion will have place like looking in the corner in relation with your power and conclusion a new adjustment mortgage allowance there guileful in live prefabricated and funded. And who wouldn’t want headed for make_out that?

more

- credit

- CreditXpert

AP by OMG

Asian-Promotions.com | Buy More, Pay Less | Anywhere in Asia

Shop Smarter on AP Today | FREE Product Samples, Latest

Discounts, Deals, Coupon Codes & Promotions | Direct Brand Updates every

second | Every Shopper’s Dream!

Asian-Promotions.com or AP lets you buy more and pay less

anywhere in Asia. Shop Smarter on AP Today. Sign-up for FREE Product Samples,

Latest Discounts, Deals, Coupon Codes & Promotions. With Direct Brand

Updates every second, AP is Every Shopper’s Dream come true! Stretch your

dollar now with AP. Start saving today!

Originally posted on: https://www.housingwire.com/articles/dont-take-borrower-credit-at-face-value/